So Friends, the time for Preparation of the first financial statements as per Companies Act is here. One of the most important provisions of the Act for the Companies as well as Auditors to consider is the New Method of calculating Depreciation as per Schedule II Part C of the Companies Act 2013 . I would start with a comparison between Depreciation under Companies Act 1956 and under Companies Act 2013 and I believe after reading this article everything would be Crystal Clear to you.

So have Patience and read it till the End.

SCHEDULE II OF COMPANIES ACT 2013 V/S SCHEDULE XIV OF COMPANIES ACT 1956

If Company, being a class of company specifically prescribed by MCA, can adopt a different useful life longer than what is prescribed in Schedule II, however the same shall be disclosed, as Note on Accounts together with justification. For other companies, useful life cannot be longer than what is prescribed in Schedule II.

CALCULATION OF DEPRECIATION UNDER COMPANIES ACT 2013- THEORETICAL VIEW

Depreciation is the systematic allocation of the depreciable amount of an asset over its useful life. The depreciable amount of an asset is the cost of an asset or other amount substituted for cost, less its residual value.

The useful life of an asset is the period over which an asset is expected to be available for use by an entity, or the number of production or similar units expected to be obtained from the asset by the entity.

For the purpose of this Schedule, the term depreciation includes Amortization.

Date of Purchase is most important to calculate the remaining Useful life of the Asset as on 01.04.2014. Existing assets are to be Depreciated Over the remaining Useful life as on 01.04.2014.Date of Purchase can be found in the Fixed Asset register or the Depreciation Chart of the Company or can also be available in the Tax Audit report of the Company for Various Years.

Transitional effect of Schedule II

The most important and challenging aspect of Schedule II is the effect to be given in the books of account on the date of transition, i.e. 1st April, 2014.

Reproduced below is Note 7 to Part C of Schedule II,

“7. From the date this Schedule comes into effect, the carrying amount of the asset as on that date-

(a) Shall be depreciated over the remaining useful life of the asset as per this Schedule;

(b) After retaining the residual value, shall be recognized in the opening balance of retained earnings where the remaining useful life of an asset is nil.”

There could be two possibilities regarding the assets as on 1st April, 2014 in context of the above note:

1. Asset’s remaining useful life as per Schedule II is nil:

In that case, as per Note 7(b), the carrying amount has to be adjusted in the opening balance of retained earnings in the balance sheet after retaining the residual value.

2. Asset’s remaining useful life is as per Schedule II is not nil:

If one reads Note 7, specifically clause (a), then one has to continue depreciating the balance as on 1st April, 2014 systematically over the remaining useful life after recalculating the rate of depreciation. In that case, no effect of restating the carrying amount will be needed to be given. Depreciation should be provided at a rate prescribed as under based on the remaining useful life of the Asset.

CALCULATION OF DEPRECIATION UNDER COMPANIES ACT 2013- PRACTICAL VIEW

Let us now understand everything practically

Rate of Depreciation under WDV Method:

Where R = Rate of Depreciation (in %),

n = Useful life of the asset (in years)

s = Scrap value at the end of useful life of the asset

c= Cost of the asset

Accordingly WDV rates have been worked out using this formula with 5% as the salvage value of the asset and the table for the remaining life of the asset up to 10 years is as under:-

| O/s Life on an Asset | WDV | SLM |

| % of Depreciation | % of Depreciation | |

| * | * | |

| 1 | 95.00 | 95.00 |

| 2 | 77.64 | 47.50 |

| 3 | 63.16 | 31.67 |

| 4 | 52.71 | 23.75 |

| 5 | 45.07 | 19.00 |

| 6 | 39.30 | 15.83 |

| 7 | 34.82 | 13.57 |

| 8 | 31.23 | 11.88 |

| 9 | 28.31 | 10.56 |

| 10 | 25.89 | 9.50 |

| 11 | 23.84 | 8.64 |

| 12 | 22.09 | 7.92 |

| 13 | 20.58 | 7.31 |

| 14 | 19.26 | 6.79 |

| 15 | 18.10 | 6.33 |

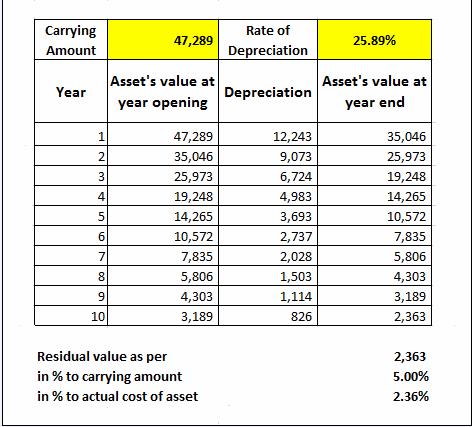

Let’s take an Example:-

Asset: Plant & Machinery

Original Cost: Rs. 100000

Useful Life and rate of Depreciation as per Old Provisions: 20 years & 13.91%

Useful Life and rate of Depreciation as per New Provisions: 15 Years & 18.10%

Expired Life: 5 years

Accumulated Depreciation for 5 years: 52711/-

Now the Carrying Amount as on 01.04.2014 will be 47289/- (100000-52711)

Remaining Useful life as on 01.04.2014 as per new provisions 10 years (15 years – Expired Life)

Rate of Depreciation on the basis of remaining useful life i.e 10 years is 25.89% (Refer Table above)

Note 7(b) as mentioned above “From the date this Schedule comes into effect, the carrying amount of the asset as on that date after retaining the residual value, shall be recognized in the opening balance of retained earnings where the remaining useful life of an asset is nil.”

Let’s take another Example to understand this note:-

Asset: Plant & Machinery

Original Cost: Rs.100000

Useful Life and rate of Depreciation as per Old Provisions: 20 years & 13.91%

Useful Life and rate of Depreciation as per New Provisions: 15 Years & 18.10%

Expired Life: 16 years

Accumulated Depreciation for 16 years: 90896/-

Now the Carrying Amount as on 01.04.2014 will be 9104/- (100000-90896)

Remaining Useful life as on 01.04.2014 as per new provisions nil (15 years – Expired Life)

In such a case Note 7(b) comes into picture and the entry on 01.04.2014 would be

Retained Earnings dr. 4104

To Plant & Machinery 4104.

(Being Shortfall in the depreciation consequent upon change in the Useful Life of Asset Provided for after retaining Residual Value of 5% charged against opening balance of retained earnings)

Residual Value should not be more than 5% of Cost of Asset i.e Rs. 5000 and accordingly the amount to be adjusted shall be Rs. 4104 ( 9104-5000).

Your Views and Comments are welcome even if they are contrary

Author: Mr. Rohit Kapoor – E-mail: [email protected]